The Data Behind India’s Digital Fraud Surge

India’s Rapid Digital Expansion

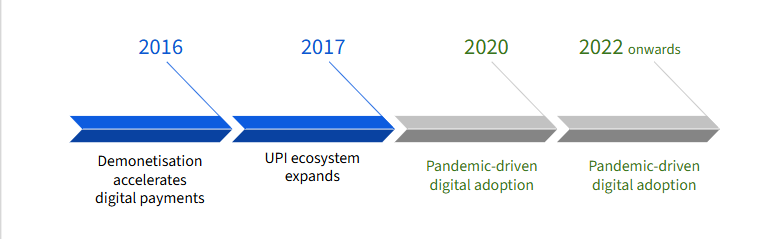

Over the past decade, India has experienced a rapid digitalisation process. The rise of digital financial services, affordable internet costs, and the penetration of smartphones have transformed the way people communicate, transact and do business online.

Online payment systems, including Unified Payments Interface (UPI), have enabled real-time transactions between banks and financial systems. As much as these systems have enhanced access to finance and efficiency, they have also created new opportunities for cybercriminals.

Cybercrime has evolved alongside the shift of financial and social interactions to digital platforms. The fraud attacks on online payments, online banking, and personal information have become common and increasingly costly.

To analyse the scale and trend of cybercrime in India, this analysis will use the datasets released by the National Crime Records Bureau (NCRB) and financial fraud data released by the Indian Cyber Crime Coordination Centre (I4C) under the Ministry of Home Affairs.

The Rise of Cybercrime in India

The Rise of Cybercrime in India

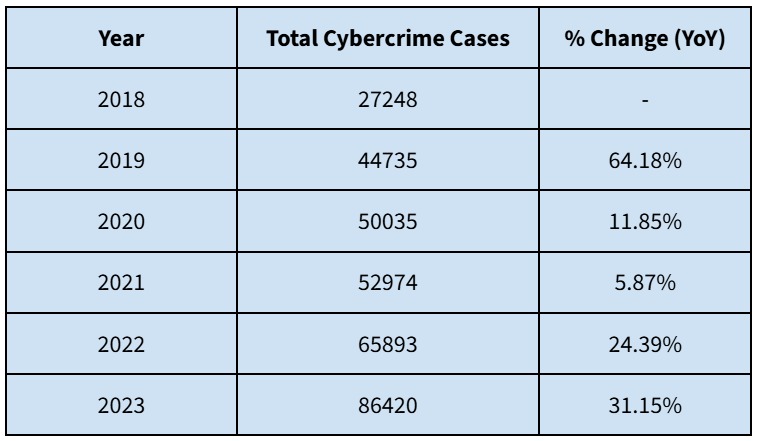

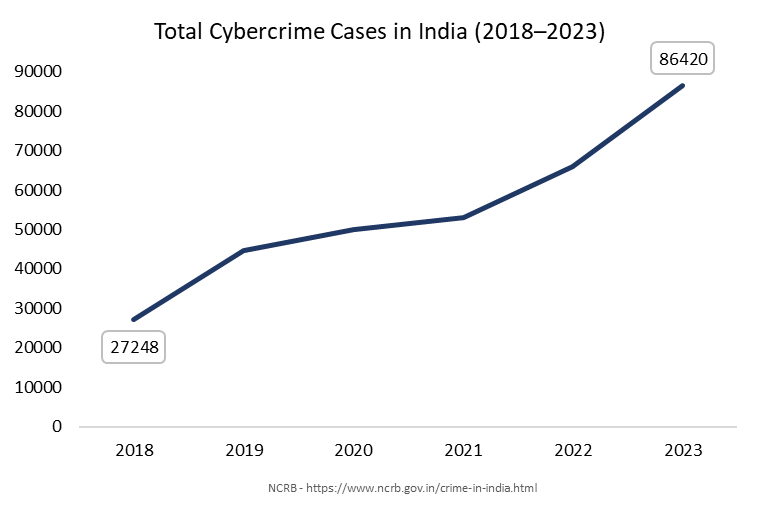

Source: National Crime Records Bureau – Crime in India Reports

The data released by the NCRB documents cybercrime incidents registered by the police at the national level under the Information Technology Act, 2000 (IT Act) and criminal provisions covering offences such as cheating, impersonation, and digital fraud. In the past, the offences were listed in the provisions of the Indian Penal Code (IPC). Following criminal law reforms in India, on 1 July 2024, the Bharatiya Nyaya Sanhita (BNS), which replaced the IPC, came into force. Section 419 (cheating by impersonation), IPC, would be related to BNS Section 319 and Section 420 (cheating and dishonestly inducing delivery of property), which would be related to BNS Section 318(4). Similarly, crimes involving forgery and use of forged documents or electronic documents, which were previously contained in the IPC Sections 465-471, are dealt with in BNS Sections 335-340.

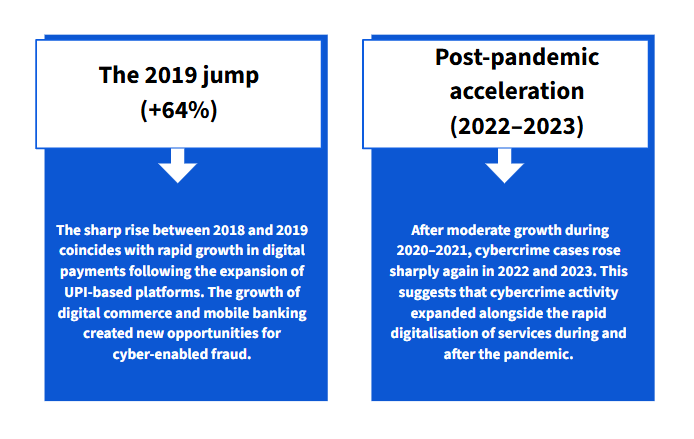

The data published by the NCRB represent the number of crimes that reached the point of the First Information Report (FIR) registration, meaning they reflect only cybercrime cases that were formally presented to the law enforcement system to investigate, rather than all complaints reported. The data shows that cybercrime cases increased from 27,248 in 2018 to 86,420 in 2023, a 3.17-fold increase in 5 years.

Two structural shifts are visible: the post-pandemic jump and subsequent acceleration.

However, these figures likely underestimate the true scale of cybercrime because many incidents are reported only through online complaint portals and may not result in FIR registration.

The Financial Scale of Digital Fraud

The Financial Scale of Digital Fraud

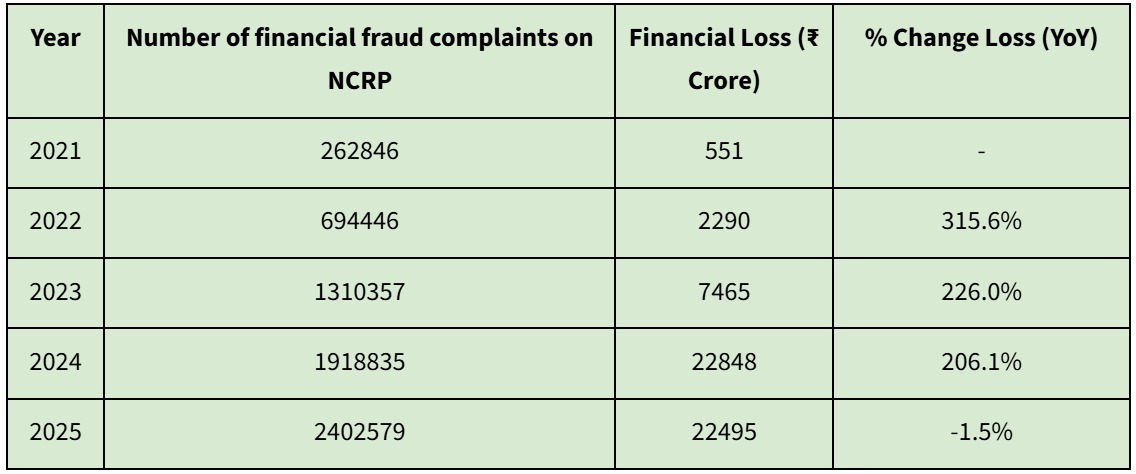

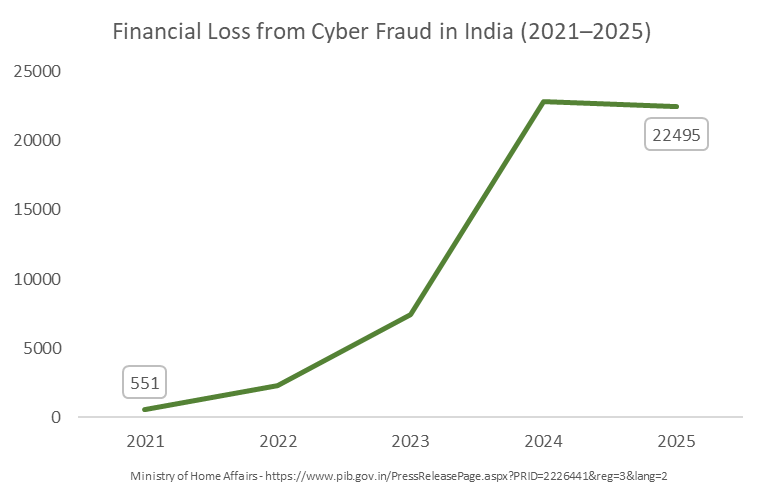

This dataset tracks financial fraud complaints reported through the National Cyber Crime Reporting Portal (NCRP) and the estimated financial losses associated with those complaints.

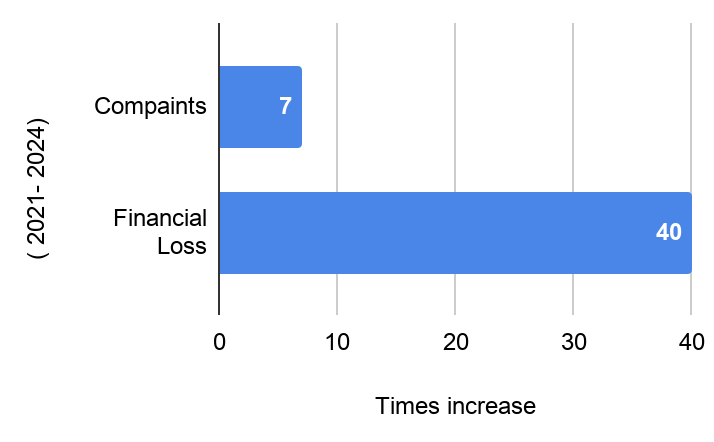

The financial losses reported between 2021 and 2024 increased by 41 times over four years, compared to 2021, from 551 crore to 22,848 crore. At the same time, the number of complaints rose from 262,846 to over 1.9 million, an increase of ~623%, indicating both rising victimisation and greater public awareness of reporting mechanisms.

The contrast between these two trends is striking:

While complaints increased by around 7 times, financial losses increased by over 40 times.

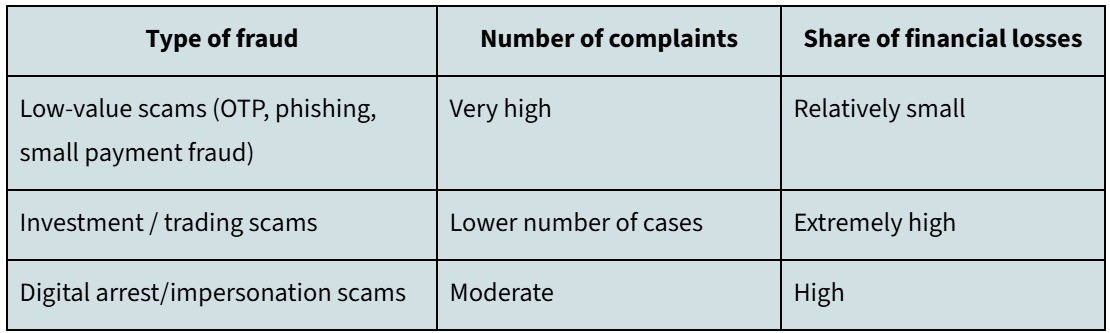

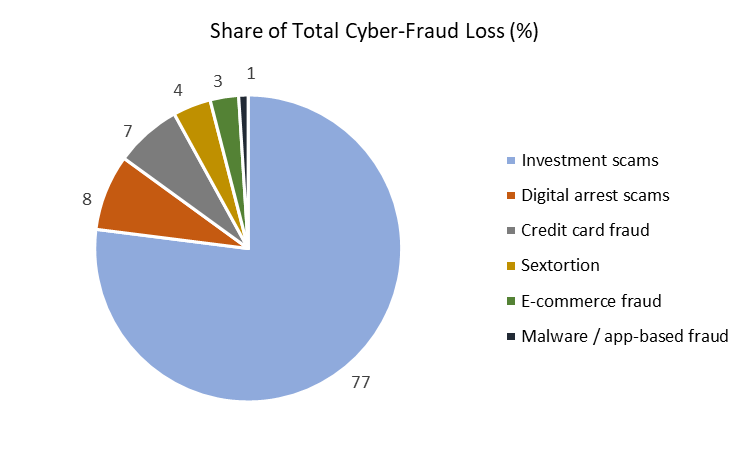

Distribution of Cyber-Fraud Complaints and Financial Losses by Fraud Type

This divergence implies an uneven relationship between the number of incidents and the financial damage that they inflict. Most cyber fraud incidents involve relatively small transaction values; however, a smaller group of fraud categories result in disproportionate numbers of financial losses.

Distribution of Financial Losses Across Major Cyber-Fraud Categories in India

As reported by The Indian Express, based on the data compiled by the I4C, investment-related scams alone account for roughly 77% of reported cyber-fraud losses, followed by smaller shares from “digital arrest” scams (8%), credit card fraud (7%), sextortion (4%), e-commerce fraud (3%), and malware or app-based fraud (1%). This distribution means that even though scams with lower values, like phishing, OTP fraud, and small payment fraud, produce a high proportion of complaints, few categories of fraud produce most of the financial losses.

Analysis

1. Cybercrime is expanding faster than most traditional crimes: The fact that cybercrime cases have tripled in five years shows that cyber offences are presently becoming a significant element of Indian crime. Unlike conventional crimes that require physical proximity, cybercrime can be conducted remotely and at scale, enabling perpetrators to target large numbers of victims simultaneously.

2. Financial losses are concentrated in a small set of fraud categories: As cases of cybercrimes have been on the increase, the monetary losses of digital fraud cases have been increasing at a higher rate. The fact that the number of reported financial losses has increased 40 times in 4 years indicates that cybercrime has a very high economic impact.

3. Complaint volumes and financial damage follow different patterns: When comparing complaints and financial losses, it is evident that cyber fraud losses are unevenly distributed across types of incidents. Most of the prevalent scams reported, including phishing or OTP fraud, involve relatively small transaction values but yield a high portion of complaints. Conversely, fewer categories of fraud, especially investment-based schemes, contribute a significantly higher percentage of total financial losses.

4. Digital financial infrastructure has expanded the attack surface: India’s rapid adoption of digital payment systems, mobile banking and digital financial systems has dramatically increased the number of potential victims of cybercriminals. The scale of online transactions creates new vulnerabilities that organised cybercrime networks take advantage of.

5. Reporting improvements reveal previously hidden crime: The expansion of national reporting systems has enhanced the transparency in the trends of cybercrime. The increase in the number of complaints recorded is partially due to improved reporting systems and not necessarily to the increased criminal activity, meaning that previous data might have understated the magnitude of cyber fraud.

Recommendations

1. Move from reactive policing to proactive cyber-risk monitoring: The conventional models of policing focus on investigation of crimes that have already taken place. With such a magnitude and pace of cyber fraud, India should have systems that are designed to detect and prevent the fraud at its early stages, such as real-time observation of suspicious patterns in transactions by financial institutions.

2. Strengthen financial intelligence sharing across institutions: There are a lot of instances of cyber fraud that use more than one bank, payment system, and telecommunication provider. To detect new networks of fraud sooner, it can be suggested to establish more information-sharing measures between the financial institution and law enforcement agencies.

3. Target organised cyber fraud networks rather than individual incidents: Many digital scams operate through organised networks that coordinate phishing, mule accounts, and fake payment channels. The solution in regard to this involves dismantling these networks through investigative procedures instead of treating incidents on a case-by-case basis.

4. Improve recovery mechanisms for stolen funds: The recovery of the funds lost is one of the most difficult issues in cases of cyber fraud. Expanding systems such as the Citizen Financial Cyber Fraud Reporting and Management System (CFCFRMS) can improve the speed at which fraudulent transactions are frozen or reversed.

5. Strengthen digital financial literacy: A significant percentage of cyber frauds are based on social engineering methods that take advantage of user behaviour as opposed to technical weaknesses. Victimisation can be greatly reduced through specific public awareness efforts on typical scam schemes.

Conclusion

India’s experience illustrates a broader global trend: as economies digitise, crime increasingly follows the flow of digital money. While cybercrime incidents are rising steadily, the much faster growth in financial losses suggests that cybercriminals are becoming more organised, technologically sophisticated, and economically motivated.

References:

- https://indianexpress.com/article/india/indians-lost-rs-53000-crore-fraud-cheating-cases-six-years-maharashtra-2025-10452185/

- https://www.pib.gov.in/PressReleasePage.aspx?PRID=2226441®=3&lang=2 -

- https://www.ncrb.gov.in/crime-in-india.html

- https://i4c.mha.gov.in/index.aspx

- https://i4c.mha.gov.in/index.aspx

Related Blogs

Introduction:

Apple is known for its unique innovations and designs. Apple, with the introduction of the iPhone 15 series, now will come up with the USB-C by complying with European Union(EU) regulations. The standard has been set by the European Union’s rule for all mobile devices. The new iPhone will now come up with USB-C. However there is a little caveat here, you will be able to use any USB-C cable to charge or transfer from your iPhone. European Union approved new rules to make it compulsory for tech companies to ensure a universal charging port is introduced for electronic gadgets like mobile phones, tablets, cameras, e-readers, earbuds and other devices by the end of next year.

The new iPhone will now come up with USB-C. However, Apple being Apple, will limit third-party USB-C cables. This means Apple-owned MFI-certified cable will have an optimised charging speed and a faster data transfer speed. MFI stands for 'Made for iPhone/iPad' and is a quality mark or testing program from Apple for Lightning cables and other products. The MFI-certified product ensures safety and improved performance.

European Union's regulations on common charging port:

The new iPhone will have a type-c USB port. EU rules have made it mandatory that all phones and laptops need to have one USB-C charging port. IPhone will be switching to USB-C from the lightning port. European Union's mandate for all mobile device makers to adopt this technology. EU has set a deadline for all new phones to use USB-C for wired charging by the end of 2024. These EU rules will be applicable to all devices, such as tablets, digital cameras, headphones, handheld video game consoles, etc. And will apply to devices that offer wired charging. The EU rules require that phone manufacturers adopt a common charging connection. The mobile manufacturer or relevant industry has to comply with these rules by the end of 2024. The rules are enacted with the intent to save consumers money and cut waste. EU stated that these rules will save consumers from unnecessary charger purchases and tonnes of cut waste per year. With the implementation of these rules, the phone manufacturers have to comply with it, and customers will be able to use a single charger for their different devices. It will strengthen the speed of data transfer in new iPhone models. The iPhone will also be compatible with chargers used by non-apple users, i.e. USB-C.

Indian Standards on USB-C Type Charging Ports in India

The Bureau of Indian Standards (BIS) has also issued standards for USB-C-type chargers. The standards aim to provide a solution of a common charger for all different charging devices. Consumers will not need to purchase multiple chargers for their different devices, ultimately leading to a reduction in the number of chargers per consumer. This would contribute to the Government of India's goal of reducing e-waste and moving toward sustainable development.

Conclusion:

New EU rules require all mobile phone devices, including iPhones, to have a USB-C connector for their charging ports. Notably, now you can see the USB-C port on the upcoming iPhone 15. These rules will enable the customers to use a single charger for their different Apple devices, such as iPads, Macs and iPhones. Talking about the applicability of these rules, the EU common-charger rule will cover small and medium-sized portable electronics, which will include mobile phones, tablets, e-readers, mice and keyboards, digital cameras, handheld videogame consoles, portable speakers, etc. Such devices are mandated to have USB-C charging ports if they offer the wired charging option. Laptops will also be covered under these rules, but they are given more time to adopt the changes and abide by these rules. Overall, this step will help in reducing e-waste and moving toward sustainable development.

References:

https://www.bbc.com/news/technology-66708571

Executive Summary

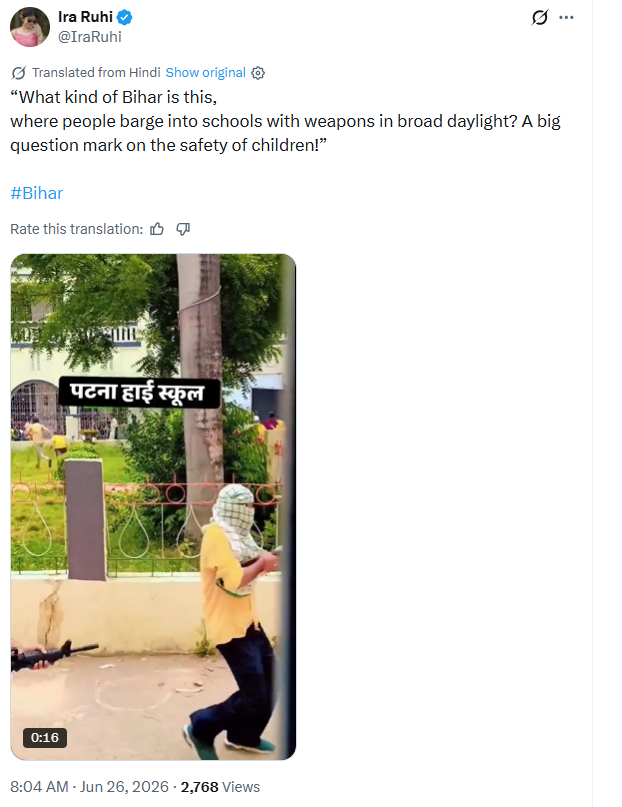

A 22-second video is circulating on social media platform X (formerly Twitter) with a claim that a shooting incident took place at Patna High School in Bihar. The video shows several masked men running around with weapons in their hands, accompanied by the sound of gunfire. A text overlay on the video reads "Patna High School." However, an research by the CyberPeace Research Wing has revealed that this claim is entirely fake and misleading. The video does not depict a real shooting; it captures an authorized movie/web series shooting on the school premises.

The Claim

Social media users are sharing the video claiming that a real firing incident occurred at Patna High School in Patna, Bihar. https://x.com/IraRuhi/status/2070334893830357499

Fact Check

Keyframes from the viral video were analyzed using reverse image search. This led to identical videos uploaded on Facebook and Instagram on June 25, 2026. The captions on both uploads explicitly stated that the footage was from a movie and web series shoot. Furthermore, a closer inspection of the videos revealed professional filmmaking equipment, such as a black flag and a skimmer, visible on the set. https://www.facebook.com/reel/2160248068089642

https://www.instagram.com/p/DaBE0gQglUF/

A targeted keyword search led to a YouTube video uploaded on June 20, 2026. The visuals in this video perfectly matched the viral footage, and the individuals seen in the viral clip could be spotted wearing the exact same clothes. "Regarding the video/photo being circulated on social media (Patna High School, Gardanibagh), it is clarified that this is part of an authorized film shooting, for which due permission was previously granted by the competent authority."

To verify further, official statements were checked. The Patna Police issued a formal press release on June 26, 2026, completely dismissing the viral rumors. https://x.com/PatnaPolice24x7/status/2070501501529960581

Conclusion

The evidence gathered confirms that there was no shooting incident at Patna High School. The viral video is behind-the-scenes footage from a pre-approved film production.

Executive Summary

A video showing a scuffle between a group of women and police personnel is being widely shared on social media with the claim that it shows Delhi Police assaulting women protesters at Jantar Mantar. CyberPeace Research Wing ’s research found the claim to be misleading. The viral video is not from Jantar Mantar in Delhi but from an unrelated incident in Dehradun, Uttarakhand. The old footage is being falsely circulated as a recent video from the ongoing protests.

Claim:

A Facebook user shared the viral video claiming that Delhi Police personnel were assaulting women and girls during the protest at Jantar Mantar.

The post link, archive link and screenshot are provided below.

https://www.facebook.com/reel/2864826433884333

Fact Check:

To verify the claim, we extracted keyframes from the viral video and conducted a reverse image search using Google Lens. This led us to the same video uploaded on the Instagram account iamvikasbaliyan on October 15, 2025.

https://www.instagram.com/reels/DP0H_SSE625/

According to the information shared with the post, the incident took place in Mohabbewala, Dehradun, Uttarakhand, after a truck crashed into a house, damaging the property. The homeowner allegedly demanded compensation and, when the issue remained unresolved, attempted to set the truck on fire. When police personnel intervened to stop her, a scuffle broke out between the woman and the police. The viral video captures this incident. In the next stage of the research, we found an ABP News report published on October 15, 2025, carrying the same visuals as the viral video. The report also identified the incident as having occurred in Mohabbewala, Dehradun.

Conclusion:

CyberPeace Research Wing ’s research found the viral claim to be misleading. The video does not show Delhi Police assaulting women protesters at Jantar Mantar. It is an old video from Dehradun, Uttarakhand, showing an unrelated incident that has been falsely linked to the ongoing protests in Delhi.